A frequent practice among expats in Costa Rica is to use a corporation to control ownership of property. However, doing so creates additional obligations under U.S. tax law.

Enacted in 2010 as part of Obama’s economic stimulus package, FATCA is designed to stem offshore tax evasion and turn foreign banks, brokerages and insurance companies into an IRS surveillance network. Foreign residents who have lawful residence in Costa Rica are tracked through their DIMEX numbers. This number is issued by immigration authorities, and when an expat opens or updates an account the number is passed along to SUGEF.

U.S. citizens are required to file taxes and report on their worldwide income. FATCA creates additional income tax filing requirements for those with assets abroad. For this, the IRS has created Form 8938, Statement of Specified Foreign Financial Assets.

Failure to report foreign financial assets on Form 8938 may result in a penalty of $10,000 (and a penalty up to $50,000 for continued failure after IRS notification). Further, underpayments of tax attributable to non-disclosed foreign financial assets will be subject to an additional substantial understatement penalty of 40 percent.

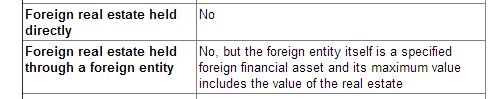

The law establishes certain thresholds, or an aggregate amount of foreign assets that trigger the reporting requirement. Normally a home or real estate would not count toward this limit. However, when the property is controlled by a corporation, it’s value is reflected in the stock held in that corporation.

The IRS says that stock in a corporation is indeed a specified foreign financial asset and is subject to FATCA reporting.

Fortunately, the thresholds are a little high to affect most retirees who live in Costa Rica full time. For example, a U.S. resident (single) has a foreign asset threshold of $50,000. A bonafide foreign resident is allowed $200,000.

However, a perpetual tourist or someone with foreign investments, who does not live abroad full time is likely to be classified as a U.S. resident for tax purposes. In these cases, people who are unable or unwilling to identify themselves as expats to the U.S. government must deal with the lower threshold.

Ignoring the FATCA requirement can get a U.S. citizen in a lot of trouble. The law itself is about reporting, and you have to file even if your business or real estate deals have lost or are not producing income. The flat $10,ooo fine is a way of penalizing those who have earned nothing on their investments, but fail to disclose them in detail for the IRS.